Financials

Quarterly Report For The Financial Period Ended 31 March 2026

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

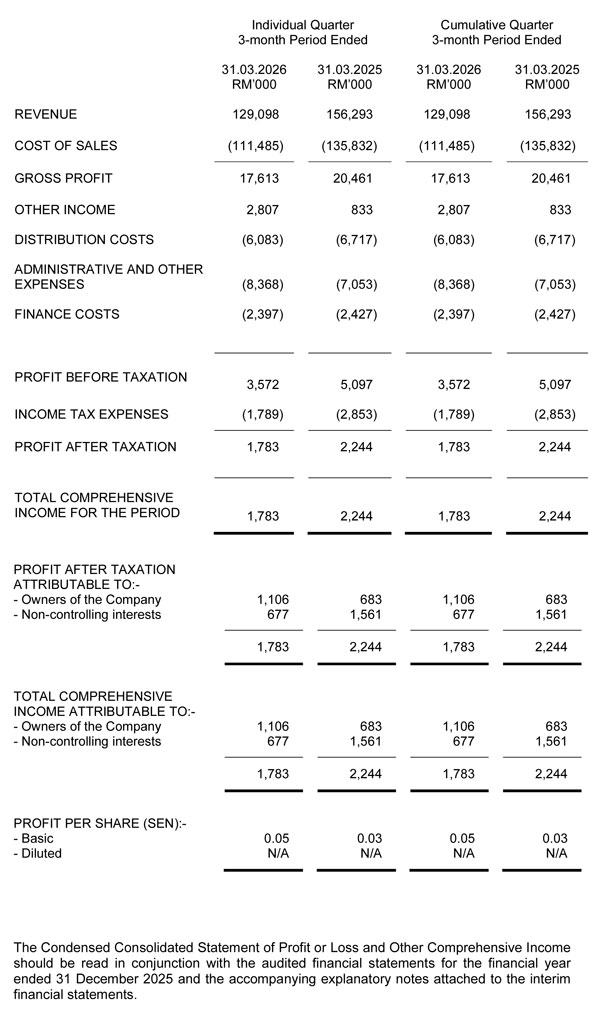

Condensed Consolidated Statement of Profit or Loss and Other Comprehensive Income

For the 1sth Quarter Ended 31 March 2026

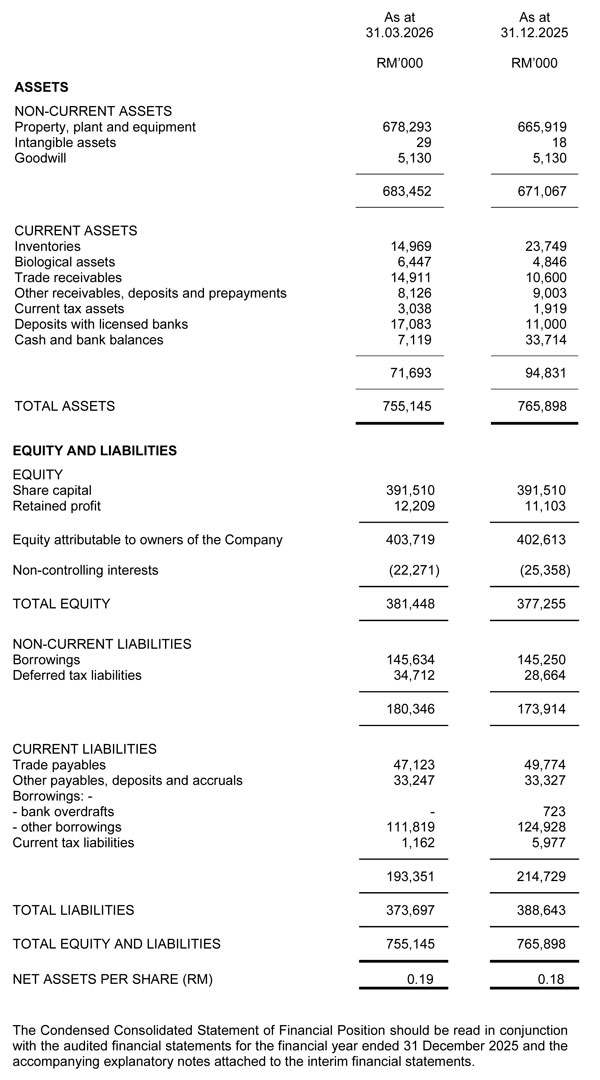

Condensed Consolidated Statement of Financial Position

As at 31 March 2026

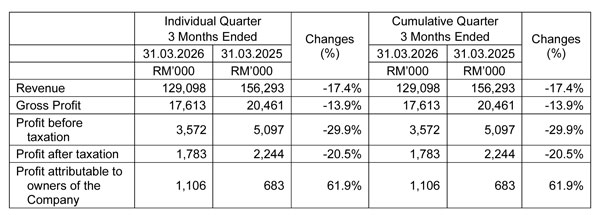

Review of performance

Financial review for current quarter and financial year to date

3 Months Ended 31.03.2026 vs 31.03.2025

For the three months ended 31 March 2026, the Group reported total revenue of RM 129.1 million, representing a 17.4% decrease compared to RM 156.3 million in the corresponding period of 2025. The sales volume for the core products increased by 15.1% for FFB, 3.0% for CPO and 5.4% for PK in the current quarter, compared with the same period in 2025. However, this increase was more than offset by a sharper decline in average selling prices, with FFB decreasing to RM782/MT (-11.4%), CPO to RM3,981/MT (-14.7%) and PK to RM3,155/MT (-7.5%), resulting in lower overall revenue.

During the quarter, cost of sales decreased by RM24.4 million, representing a 17.9% decline. This included the lower FFB processed cost, windfall levy, and plantation administrative expenses. Nevertheless, the decrease was partially offset by rise in manuring costs, depreciation and amortisation expense and transportation costs. Consequently, gross profit declined by RM 2.8 million to RM17.6 million from RM20.5 million in the same period last year. The decline in revenue was partly cushioned by higher fixed deposit interest income and a gain arising from changes in the fair value of biological asset. Hence, profit before taxation and profit after taxation decreased by RM 1.5 million (-29.9%) to RM3.5 million and by RM 0.5 million or 20.5% to RM1.8 million, respectively.

The income tax expense for the quarter was lower by 37.3% or RM 1.1 million compared with the corresponding period of 2025. As a result, profit attributable to the owners of the Company increased by 61.9% to RM1.1 million.

Commentary on Prospects

The Malaysian oil palm industry entered 2026 with a favorable outlook, supported by stronger crude palm oil (CPO) prices, declining inventories, resilient export demand, and improving regional biodiesel mandates. CPO prices remained firm at elevated levels compared with historical averages, providing stronger revenue and margin support for plantation companies, particularly upstream producers. Lower inventory levels in Malaysia, driven by exports outpacing production growth, further strengthened market sentiment and reduced downward pressure on prices. Export demand from key consuming markets such as India, China, and other importing countries remained supportive, contributing positively to overall industry performance in the first quarter.

Prospects remain constructive although market volatility is expected. CPO prices are likely to stay relatively firm, supported by biodiesel demand, currency movements, and global vegetable oil market dynamics. However, seasonal recovery in fresh fruit bunch (FFB) production may increase supply moderately and cap further price upside. Despite this seasonal improvement, Malaysia continues to face structural constraints including labour shortages, ageing palm tree profiles, slower replanting activities, and limited land for expansion, which are expected to prevent excessive production growth and continue supporting prices.

Overall, the outlook for the Malaysian oil palm industry is positive. Earnings momentum should remain healthy in the first half of the year, particularly for efficient upstream plantation companies with strong yields, cost discipline, and high oil extraction rates. Integrated players with refining and downstream exposure may also benefit, although margins could be more mixed depending on feedstock costs. The industry remains fundamentally supported, but companies must continue focusing on productivity improvement, cost control, mechanization, and prudent selling strategies to maximize returns.